For decades, Uganda’s motorists played a dangerous game by buying cheap fake insurance stickers from a street vendor, hoping the police don’t look too closely and pray you never have to make a claim.

Now, a simple WhatsApp bot is dismantling that entire shadow market one message at a time.

On many roads across Uganda, the old ritual is fading and with motorists used to pulling over at a roadside stall, hands over a few thousand shillings, and in return receives a flimsy, brightly coloured sticker and it looks like insurance having a policy number, a logo, even a fake hologram but when the moment of truth comes an accident, a police checkpoint, a serious claim it is worth nothing.

In addition, for years, counterfeit motor third-party insurance stickers thrived in Uganda and they exploited a system built on paper, physical inspections and manual verification with fraudsters simply copying genuine stickers, sold them at half the price, and disappeared and drivers who bought them thought they were covered yet they were not.

However, that era is ending not with a complex smartphone app requiring data and tech literacy, but with a tool almost every Ugandan already has in their pocket – WhatsApp.

Excel Insurance, working with technology partner Service Cops, launched a WhatsApp bot in 2024 that has quietly revolutionized how motor insurance is bought, verified and enforced.

Additionally, this is not a glitzy product that wins awards for innovation though it did earn recognition in the 2025 industry awards season and it is something arguably more powerful; a practical, accessible solution that is dismantling a counterfeit economy and bringing the informal sector into the formal insurance net.

Motor third-party insurance is not optional in Uganda but rather it is a legal requirement, designed to ensure that victims of road accidents can claim compensation for injury or death and yet for years, enforcement was nearly impossible.

However, this was because the old system relied on physical stickers affixed to windscreens and police officers at checkpoints would glance at the sticker, maybe check the date, and wave the driver through with counterfeiters flooding the market with replicas so convincing that even experienced officers could be fooled.

According to the insurance industry estimates, a significant portion of vehicles on Ugandan roads carried fake stickers at any given time and drivers who bought them saved a few thousand shillings and gambled with the financial security of everyone they might crash into.

“A fake sticker is not just a fraud against the insurer, and it is a fraud against every road user and if that driver causes an accident, there is no cover and the victim is left with nothing,” says Alhaj Kaddunabbi Ibrahim Lubega, Chief Executive of the Uganda Insurance Regulatory Authority (IRA).

“IRA had long sought a solution and the turning point came with a decision to go digital; and here we are,” he added.

In 2023, the IRA announced a phased transition from physical insurance stickers to an electronic system and the goal was simple: create a central database where every valid policy is recorded, and give police the tools to check it instantly.

In 2023, the IRA announced a phased transition from physical insurance stickers to an electronic system and the goal was simple: create a central database where every valid policy is recorded, and give police the tools to check it instantly.

The new system, managed by Service Cops, equips traffic officers with handheld scanners and at a checkpoint, an officer can now scan a vehicle’s registration plate and immediately see whether it has valid insurance live, with no room for forged stickers or expired papers.

However, digitizing the verification system only solved half the problem with the other half making it easy for drivers to buy legitimate insurance in the first place and if the purchase process remained cumbersome, many would still turn to the informal market.

A conversation, not an app

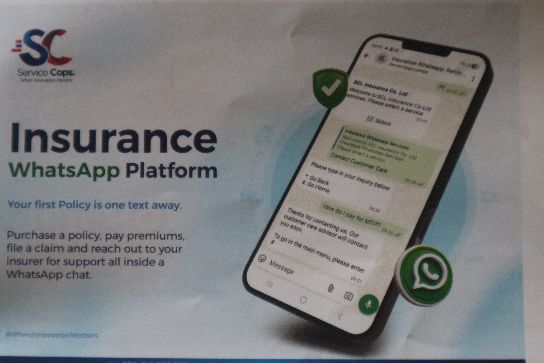

Excel Insurance is a Ugandan insurer with a long history in motor underwriting and when the IRA announced the digital shift, the company saw an opportunity to reimagine the customer experience not by building a sophisticated mobile app, but by meeting customers where they already are.

WhatsApp is ubiquitous in Uganda and it is used for business, family communication, even banking and Excel realized that a WhatsApp-based purchasing bot could be more effective than any standalone application.

According to UCC, Annual Communications Sector Report 2024, mobile subscriptions surpassed the 40 million mark and internet users exceeded 15 million and by the third quarter of 2025, these figures had risen significantly.

The report further revealed that active mobile subscriptions (90-day activity) grew to 45.7 million while mobile internet subscription reached 17 million with mobile money subscriptions climbed to 35.6 million and smartphone ownership expanded to 19.0 million devices.

Further, UCC’s report highlighted that social media usage continued to grow and as of September 2025, WhatsApp remained the most widely used platform with 10 million subscribers followed closely by TikTok at 9.3 million, YouTube at 6.3 million, Snapchat at 2.5 million, Instagram at 1.3 million and X at 0.7 million.

Therefore, the bot, developed in partnership with Service Cops, allows a customer to buy motor third-party insurance entirely through a WhatsApp conversation and the user types a few messages, selects coverage, pays via mobile money, and within seconds receives an electronic certificate and confirmation. No office visit. No paperwork. No physical sticker.

Therefore, the bot, developed in partnership with Service Cops, allows a customer to buy motor third-party insurance entirely through a WhatsApp conversation and the user types a few messages, selects coverage, pays via mobile money, and within seconds receives an electronic certificate and confirmation. No office visit. No paperwork. No physical sticker.

“We deliberately chose WhatsApp because it is already in the hands of Ugandans; you do not need to download a new app, create a password, or learn a new interface and you just have a conversation,” explains a representative from Excel Insurance.

Further, the bot also eliminates the middlemen who historically sold fake stickers and with direct access to the insurer, drivers can buy coverage at the official price, confident that their policy is recorded in the national database.

For Excel, the benefits are clear with lower distribution costs, real-time customer data, and dramatically reduced fraud, and for customers, the benefits are equally tangible with convenience, transparency, and peace of mind.

At a police checkpoint on the Kampala-Jinja highway, a traffic officer stops a taxi; the driver, Ssebunya [Not Real Name], bought his insurance through the Excel WhatsApp bot just hours earlier and the officer pulls out a handheld scanner, points it at the vehicle’s registration plate, and a green confirmation appears on the screen hence, a valid insurance and Ssebunya is waved on.

“Before, I used to buy stickers from the side of the road, and sometimes they were real, sometimes fake; I never really knew and now I buy through WhatsApp, pay with my phone, and I know I am covered and when the police scan, there is no problem,” he says.

Thus, the combination of digital purchase and digital verification has closed the loop with the fake sticker market, once thriving is being starved and drivers who try to cheat the system are caught immediately with their plates flagged as uninsured.

“The beauty of the system is that it is self-reinforcing,” says a spokesperson for Service Cops. “If a driver is not in the database, they are caught. They cannot claim ignorance because the purchase channel is so simple. Over time, more and more drivers are coming into the formal system.”

A model for the region

What started as a practical solution to a local problem is now being watched across East Africa with Kenya, Tanzania and Rwanda all grappling with similar challenges of counterfeit insurance and manual enforcement. Uganda’s WhatsApp bot and digital verification system offer a template that could be adapted elsewhere.

Uganda’s model combining real-time digital verification with accessible, mobile-based purchasing offers more than a fix to a local problem but it presents a scalable blueprint for reforming insurance markets across Africa, where low penetration, weak enforcement and public mistrust have long undermined the sector.

“In Africa, where insurance penetration is still low, innovation must be seen as a tool for financial inclusion,” says Dr, Joseph Buturo, Secretary General of the Burundi Insurance Control and Regulatory Agency.

“In Africa, where insurance penetration is still low, innovation must be seen as a tool for financial inclusion,” says Dr, Joseph Buturo, Secretary General of the Burundi Insurance Control and Regulatory Agency.

“It must reach rural populations, small farmers and small businesses with people who have traditionally been excluded,” Buturo added.

Buturo argues that the real breakthrough in Uganda is not simply digitisation but it is accessibility and by embedding insurance into a familiar platform like WhatsApp, the system removes long-standing barriers such as distance to offices, paperwork and lack of awareness.

“This is how you bring insurance closer to the people and when services are simple, transparent and immediate, trust begins to grow,” he adds.

He further argues that trust is the foundation on which insurance markets either succeed or fail and with innovation which is an essential strategic lever to strengthen confidence and respond to new risks like climate, health and technological barriers; these challenges that are common across the region need collective responses.

He further argues that trust is the foundation on which insurance markets either succeed or fail and with innovation which is an essential strategic lever to strengthen confidence and respond to new risks like climate, health and technological barriers; these challenges that are common across the region need collective responses.

He, however, points to the need for deeper regional cooperation not just in sharing technology but in harmonizing regulatory frameworks, integrating databases and enabling cross-border verification systems.

“Sharing experiences and pooling knowledge will accelerate progress and no country can solve these challenges in isolation,” he emphasized.

On the other hand, Dr. Baghayo Abdallah Saqware, Commissioner of Insurance & Head of the Tanzania Insurance Regulatory Authority (TIRA) frames the issue more bluntly, citing that access is not enough but uptake is the real test.

“One of the biggest challenges in Africa is access and uptake; what will we do to expand access? What will we do to encourage uptake? Innovation becomes inevitable,” Dr. Saqware said.

Saqware argues that while digital tools like Uganda’s WhatsApp bot remove logistical barriers, they must be paired with deliberate efforts to build public confidence in insurance systems.

“People must understand and accept these solutions and technology can open the door but trust is what brings people inside,” he noted.

He further suggests several practical steps embedding insurance education into digital platforms using vernacular languages in bots and messaging and integrating insurance services with everyday financial tools like mobile money and savings groups.

“We must move from passive systems to proactive ones and the insurer should not wait for the client to chase a claim but the system should trigger responses automatically,” Saqware disclosed.

Therefore, the shift from reactive to proactive service is where Uganda’s model could evolve next and with a centralized database already in place, insurers and regulators have an opportunity to build additional layers with automated claims alerts, integration with hospital systems for injury reporting and even predictive analytics to identify high-risk drivers and reduce accidents.

Back in Uganda, the early signs of transformation are already visible with roadside vendors selling questionable stickers are now disappearing, squeezed out by a system that is faster, cheaper and far harder to manipulate; and traffic officers no longer rely on visual checks but on real-time data and drivers increasingly are choosing certainty over shortcuts.

In addition, for motorists, the gamble is ending not just because enforcement is tighter but because compliance has finally been made convenient.

Therefore, for the insurance industry, the implications go far beyond motor cover but the same model-simple digital access paired with strong verification could be applied to health insurance, agricultural cover and micro-insurance products targeting underserved populations.

In that sense, Uganda’s WhatsApp bot is not just fixing a broken system but it is redefining how insurance can work in Africa not as a distant, bureaucratic obligation but as an everyday service that is accessible, reliable and trusted; hence, if that trust holds, the transformation now visible on Uganda’s roads may soon extend far beyond them.

For IRA, the success of the initiative has broader implications and it demonstrates that digital transformation in insurance does not require cutting-edge apps or complex infrastructure but rather it requires understanding how people actually live and meeting them there.

“Technology is only effective if people use it and WhatsApp is simple, trusted and widely used; that is why it works,” says Lubega.

In addition, the regulator is now exploring how similar approaches could be applied to other insurance products like health, agriculture, even micro-insurance for informal workers and if the motor insurance experience can be simplified to a WhatsApp conversation, why not other forms of protection.

Challenges remain

However, the transition is not without obstacles and some older drivers remain unfamiliar with digital tools especially in rural areas with limited mobile network coverage still struggle to access the system and there are concerns about data privacy and the concentration of customer information in the hands of a few platforms.

Excel Insurance and Service Cops have responded by maintaining traditional channels alongside the digital option, ensuring that no driver is left behind and the bot also includes simple, text-based prompts that work on basic phones, not just smartphones.

Below is the National Backbone Infrastructure (NBI) Coverage map showing completed & planned fibre developments.

The fraudsters who once thrived on fake stickers have not disappeared overnight. Some have moved to new scams but the core market for counterfeit motor insurance has been decisively disrupted.

The fraudsters who once thrived on fake stickers have not disappeared overnight. Some have moved to new scams but the core market for counterfeit motor insurance has been decisively disrupted.

However this bot has made insurance accessible to thousands of drivers who previously found the process intimidating and it has given police a tool that actually works showing that digital transformation in Africa does not have to copy Western models but it can build on what is already here.

Therefore, for the driver stopped at a checkpoint on a dusty highway, none of that theory matters but what matters is the green light on the scanner screen, the confirmation that they are covered, and the knowledge that the sticker on their windscreen or rather, the data behind it is finally real.

Thus, the Excel Insurance WhatsApp bot is not a flashy product with a slick presentation and it is, in many ways, mundane: a bot that handles routine transactions, a scanner that checks plates, a database that records policies.

Discover more from tndNews, Uganda

Subscribe to get the latest posts sent to your email.